The Next Half Billion (NHB) represents the second major wave of internet users in India. Unlike the first wave, which primarily consisted of upper and middle-income households, the NHB primarily come from lower-income households, with the majority having little to no prior digital engagement. As they come online, they face unique challenges that shape their digital experience.

One of the most pressing concerns for the NHB is their limited trust in digital services due to concerns about online safety. While by 2021, 96 percent of Indian households had a bank account, high dormancy rates persist. India’s Unified Payments Interface (UPI) is likely the first layer of contact the NHB has with the digital ecosystem, enabling subsequent access to credit, insurance, and investment products. However, over 50 percent of the NHB have encountered at least one instance of fraud, harassment, bullying, reputational harm, negative self-image, misinformation, or downloading a fake app. Financial fraud is particularly significant, with 24 percent of victims losing Rs. 2000 or more, and 3 percent losing Rs. 12,000 or more. Given these risks and their already limited trust in digital financial services, building trust among the NHB in a fast-growing digital financial services ecosystem is essential. Thus, without meaningful efforts to improve trust in Digital Financial Services (DFS) among the NHB, adoption may remain limited, preventing them from fully benefiting from financial inclusion.

- Adoption of Digital Financial Services

Digital financial services are financial services that rely on digital technologies for their delivery and use by consumers. DFS has the potential to reduce friction in accessing financial services; it can thus lead to scale efficiencies, lower transaction costs and increase the speed, security, and transparency of transactions. Access to affordable digital financial services can contribute to poverty reduction and economic growth, thus, making DFS an effective tool for advancing financial inclusion.

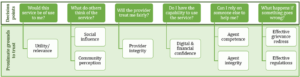

Frameworks for understanding trust in DFS focus on key “decision points” that influence customer trust during the adoption of digital financial services. These include questions about the utility of the service, social influence, the perceived fairness of the provider, a user’s digital and financial confidence, agent competence and integrity, and grievance mechanisms. Thus, trust is shaped by perceptions of whether the service is relevant, beneficial, transparent, secure, and backed by a trustworthy community.

Frameworks for understanding trust in DFS focus on key “decision points” that influence customer trust during the adoption of digital financial services. These include questions about the utility of the service, social influence, the perceived fairness of the provider, a user’s digital and financial confidence, agent competence and integrity, and grievance mechanisms. Thus, trust is shaped by perceptions of whether the service is relevant, beneficial, transparent, secure, and backed by a trustworthy community.

Source: Dvara Research

IIMA Ventures’ research characterises trust as a psychological state that operates under conditions of risk and interdependence, where the trustor believes that the trustee will fulfill their expectations without exploiting their vulnerabilities. The perception of “trustworthiness” is often judged based on the credibility and capability of the entity in delivering on its promises.

Financial relationships are particularly prone to uncertainties and a lack of trust. This can be attributed to cognitive overload, where individuals struggle to process complex financial information, and a lack of control over their financial interactions due to the added complexity of navigating layers of technology. This creates psychological and technical barriers to trust, making it a significant factor in the adoption of digital financial services.

In the context of digital payments, building trust is essential to overcoming these barriers. Individuals must believe that digital financial systems are credible, secure, and capable of protecting their interests. If users lack confidence in the reliability, security, or fairness of a system, they may hesitate to adopt digital payments, preferring traditional cash transactions instead.

2. India Case Study

Digital Public Infrastructure (DPI) is an approach to addressing socio-economic problems at scale by combining open technology components with robust governance to encourage public and private innovation. India’s UPI is an example of the role of DPI in the development of an inclusive open finance network. It is a real-time payment system enabling instant fund transfers via mobile apps of banks or third-party apps, is a compelling case to understand how fostering trust may help achieve widespread adoption and digital financial inclusion. The rapid growth of UPI–from 17.9 million transactions in 2016 to 172 billion in 2024–demonstrates its transformative impact. However, despite large transaction volumes, financial inclusion may not be as deep as it appears.

When engaging with digital payments, users must feel confident that their money is secure. If scams become too frequent, their willingness to conduct digital transactions diminishes, ultimately slowing the growth of digital financial services. This erosion of trust could hinder the broader benefits of financial inclusion and economic growth that digital payments aim to achieve. For many users, a trust deficit could also emerge from low digital or financial capabilities, making them hesitant to transition from cash to digital payments. On the supply side, trust issues stem from concerns about product reliability, provider credibility, and regulatory protections. If left unaddressed, these entrenched perceptions may weaken confidence in digital financial services, discouraging new users, slowing adoption, and adversely impacting India’s financial inclusion objectives.

Fostering greater trust may be achieved by strengthening security in the design of the system, ensuring the grievance redressal mechanism is robust, and ensuring that financial and digital literacy initiatives empower individuals to not only trust the system but also their own ability to navigate it.

Designing systems for trustworthy payments

India’s retail payment landscape remains largely dominated by cash, reflecting deep-rooted cultural and behavioral preferences. Many individuals, particularly in lower-income groups, continue to rely on cash transactions because their sources of income are cash-based, and they see little need to maintain a digital account. Studies by USAID have found that a key reason for this reluctance is a lack of confidence in digital financial services. Users worry about security risks, hidden costs, and potential transaction failures, making them hesitant to transition away from cash.

Despite efforts to expand digital financial inclusion, many digital payment systems are not designed with these users in mind. Fintech companies and global tech firms have led innovation in the sector, but much of this progress has focused on wealthier, urban populations. Since these innovations depend on existing banking infrastructure, outreach to lower-income and marginalised users remains limited. As a result, many people who could benefit from digital payments remain excluded, reinforcing distrust in the system.

For digital financial services to reach and gain acceptance among this population, they must be seen as secure, reliable, and user-friendly. Perceived credibility—the belief that providers and systems operate with integrity—is essential. Unlike in traditional banking, where individuals can ask questions in person, digital services often leave users with little opportunity to clarify doubts. Any uncertainty about data protection, transaction reliability, or hidden fees can discourage adoption. Designing digital payment systems that explicitly account for the needs and concerns of lower-income users may encourage the NHB to adopt DFS. As an effort to achieve this, UPI has been integrated into feature phones, is offered in multiple local languages, and has voice-based applications to make payments accessible to a wider population. However, additional efforts can be undertaken. For instance, app download and installation pathways should be simplified as intuitive user experiences help enhance accessibility. Designing systems that consider users with basic digital skills is crucial for enhancing the user experience. This can be achieved through in-person support and straightforward language. Moreover, in-app privacy and user controls can help promote transparency and autonomy which is also an important component to enhance and support the user experience. Ensuring that users have all the information that they need and feel secure as they interact with the application is key.

Strengthening grievance redressal mechanisms to build trust

While UPI’s instant payment feature has been a key driver of its success, it has also made addressing scams and dispute resolution more challenging. Despite existing safeguards, these scams evolve rapidly and system vulnerabilities are exploited through phishing, fake payment links, and impersonation of trusted entities. The prevalence of scams has escalated significantly, with 4.85 billion rupees lost in FY2025.

Given that scams are constantly evolving, strengthening grievance redressal mechanisms (GRMs) is critical to maintaining user trust. A 2023 report by Dvara Research in 2023 found that existing GRMs were poor due to high rates of rejection, delays, and unsatisfactory resolutions. When users struggle to report or escalate issues effectively, due to the absence of effective redress mechanisms, they may perceive the system as unreliable and unsupportive which may trigger distrust. This lack of confidence and trust disproportionately affects rural and digitally illiterate individuals, who may choose to stop using UPI altogether rather than risk financial loss without a clear path to resolution.

In-app GRMs, which serve as the first point of contact for users facing issues, often fail to meet expectations. Many apps do not prominently display complaint options, making it difficult for users to access help when required. Some apps lack in-app grievance mechanisms altogether, forcing users to navigate complex external processes. Moreover, the report highlighted other shortcomings such as inadequate support in vernacular languages, the absence of dedicated sections for non-payment complaints, and difficulty in tracking complaint statuses. These challenges weaken trust in the system.

To foster trust and encourage adoption by the NHB, UPI’s grievance redressal framework should also be made more accessible, efficient, and user-centric. This includes streamlining in-app GRMs, ensuring they are easy to locate, providing multilingual support, and offering clear escalation paths. By strengthening these mechanisms, users will feel reassured that their concerns are important and addressed promptly and fairly, reinforcing their confidence in digital financial services.

Bridging the digital literacy gap to build trust

Expanding digital financial services to India’s Next Half Billion—a group largely composed of rural residents with lower education and literacy levels—presents a unique trust challenge. Unlike India’s first wave of internet users, many in this segment have limited or no prior exposure to digital systems. Without foundational digital literacy, these individuals may struggle to navigate digital payments, increasing their vulnerability to fraud and errors. A significant barrier to adoption is distrust—research indicates that nearly one-fifth of NHB individuals cite distrust in their own abilities as a reason for avoiding digital financial services. To ensure that UPI achieves widespread adoption, it must not only be accessible but also instill confidence in users, ensuring users trust their ability to engage in digital transactions.

Financial literacy is defined not only as the ability to understand financial services but also the confidence to apply the knowledge to make effective financial decisions. Digital literacy is the knowledge and ability to manage information through digital devices. Financial illiteracy can be a barrier to financial inclusion as a lack of skills and knowledge may discourage individuals from using financial services. Similarly, digital illiteracy may prevent users from appropriately understanding or using digital technologies. Thus, financial and digital illiteracies may adversely impact digital financial inclusion.

To build financial literacy, training courses and coaching through one-on-one meetings with loan officers may allow users to receive valuable education about access to credit, its purpose, implications, and utilization. To build digital literacy, users must understand how digital systems work, the benefits they offer, the risks they may encounter, and mechanisms to mitigate these risks. The purpose is to build user confidence in their ability to navigate digital systems. This can be achieved through educational initiatives and the presence of dedicated support teams. Building both digital and financial literacy may build trust and increase user security and capability when managing digital financial transactions. This may encourage adoption and drive deeper financial inclusion.

3. The way forward: A global consensus on improving trust

Trust has become a central theme in global discussions, particularly in the context of digital public infrastructure. The Safeguards Framework emphasises the role of trust in the successful adoption and sustainability of DPI. Trust is not just a desirable attribute but a critical necessity for ensuring that individuals, communities, and institutions willingly engage with DPI systems. A lack of trust—whether in government institutions, digital systems, or the broader regulatory framework—poses a significant normative risk which can reduce users’ willingness to engage with and benefit from the specific DPI. Rather than prescribing rigid solutions, the framework underscores the need for contextual understanding—acknowledging that trust is shaped by local histories, governance structures, and societal expectations.

The Safeguards Framework identifies trust deficits as stemming from structural vulnerabilities such as digital distrust, weak rule of law, fragile institutions, technical shortcomings, and concerns over long-term sustainability. For instance, it states that the lack of independence in data-protection authorities, audit bodies, and agencies is a critical issue that can erode user trust and legitimacy. Without independent oversight, concerns over accountability and transparency persist, deterring public confidence in DPI. Additionally, the absence or inadequacy of effective remedies and redress mechanisms leaves individuals affected by DPI risks without means to mitigate harms. If people feel they have no recourse when digital systems fail or cause harm, their trust in DPI diminishes further.

Moreover, when users fear surveillance, data exploitation, exclusion, or discrimination, and/or are not safeguarded against these risks, it can exacerbate existing societal inequities and reinforces distrust. Each of these factors can erode public trust, ultimately reducing the willingness of individuals to interact with digital services and undermining the legitimacy, effectiveness, and adoption of digital transformation efforts.

To mitigate the adverse impact of trust on DPI adoption, the Safeguards framework states that trust must be embedded at every stage of the DPI lifecycle, from design to implementation and maintenance, ensuring that systems remain secure, transparent, and responsive to users’ needs. Ultimately, DPI can only drive equitable and inclusive digital transformation if trust is actively built, strengthened, and maintained. However, the framework maintains that no single blueprint can dictate how trust should be built or maintained; instead, nations must learn from one another, sharing insights on what has worked and what has not. In a rapidly evolving digital landscape, the ability to foster trust will define the success of DPI.

References

- Chandra, K., et al. (2024). From Brasilia to Bombay: The Unlikely Twins Leading A Global Open Finance Revolution. Centre for Digital Public Infrastructure.

- Dalberg. (2024). Digital Access and Beyond. How being online is impacting India’s Next Half Billion Users.

- Koefer, F., et al. (2024). Addressing Financial and Digital Literacy Challenges for Inclusive Finance: Insights from Microfinance Institutions and FinTech Organisations. EIF Research and Market Analysis.

- Kulkarni, A., Ashraf, H., & Ghosh, I. (2023). Part 2 – Is Lack Of Trust Keeping Customers Away From Digital Financial Services? Understanding The Countours Of Trust. Dvara Research.

- Narayan, A., & Prasad, S. (2023). Do UPI In-App Grievance Redress Mechanisms work for constrained users? Dvara Research.

- Pazarbasioglu, C., et. al. (2020). Digital Financial Services. World Bank Group.

- Sharma, S., Ghoshal, T., & Basoya, S. (2020). Design for Bharat: Solving for Mistrust in Digital Financial Services. IIMA Ventures.

- Waghmare, A. (2025). Access to banking. Data for India.